PhD, CFEI®

About The College Press

College to Host 11th Annual Military Summit

KING OF PRUSSIA, Pa. — August 27, 2025 - The American College of Financial Services will host its 11th annual Military Summit in Philadelphia on Sept. 18, 2025, coinciding with the 13th anniversary of the founding of the American College Center for Military and Veterans Affairs.

The event, hosted by the Center for Military and Veterans Affairs, will bring together members of the military community, financial professionals and supporters to honor veteran scholars, celebrate donors and partners, and provide professional development opportunities.

“We strive to create an environment where service members, veterans, and their spouses feel seen, supported, and equipped for long-term success,” said Phil Easton, retired CMSgt, USAF, managing director of the Center. “The Military Summit is about more than recognition; it's about offering meaningful access to education, career advancement, and a community that understands and champions the military journey.”

A highlight of the Military Summit will be the presentation of the Soldier-Citizen Award to retired Navy Vice Adm. James Zortman during a formal dinner at the National Constitution Center. A U.S. Naval Academy graduate, Zortman served 34 years in the Navy, commanding at the highest levels and earning numerous top honors. Since retiring in 2007, he has led in the private sector and currently serves as chairman of the board for USAA, supporting the financial well-being of the military community.

“I’m deeply honored to be selected for the Soldier-Citizen Award,” Zortman said. “Partnering with The American College of Financial Services and its sponsors reflects our shared dedication to those who have served. I’m eager to take part in an event that highlights the impactful work The Center is doing for the military community and the academic success of military affiliated scholars.”

The summit underscores The College’s commitment to the Center’s mission of empowering those who serve, supporting military members and their spouses through career transitions via educational and employment opportunities in the financial services sector. The event will include:

- An invite-only networking lounge for military resource groups (MRGs) and scholars.

- Dynamic discussions and workshops focused on leadership and key topics in the financial services industry that will qualify for American College Professional Recertification CE credit. Highlights include the Maury Stewart Lecture Series, featuring a marquee speaker session with Rebecca Patterson, educational workshops such as “Surprising Optimism in Retirement” with Michael Finke, PhD, CFP®, and a fireside chat on “Lessons in Leadership” with Zortman.

- The scholarship fund dinner at the National Constitution Center, honoring Zortman as the 11th annual Soldier-Citizen Award recipient and celebrating the veteran scholars and supporters who advance The College’s mission.

Join us in Philadelphia to celebrate veterans, learn from experts, and network with professionals committed to supporting the military community. For more information, visit https://events.theamericancollege.edu/military-summit-2025.

For more information, contact:

Jared Trexler

610-526-1268

jared.trexler@theamericancollege.edu

Sarah Tremallo

908-967-0381

Stremallo@jconnelly.com

About The American College of Financial Services

The American College of Financial Services is the nation’s largest nonprofit and accredited educational institution devoted to financial services professionals. Nearly one in five advisors or agents is an alum of The College. The College offers a learning platform that includes professional designation, certification, and degree programs and encompasses early-career foundational knowledge as well as deep, specialized education in tax, retirement income, philanthropy, risk management, and more with the highest-quality combination of rigor and relevance. The College’s faculty represents the foremost thought leaders in the financial services industry. Its educational programs, research, and events offer professionals the opportunity to accelerate through knowledge, grow through connections, and uplift through community.

Visit TheAmericanCollege.edu to discover all the ways you can expand your opportunities with The College.

PhD, CFP®, MSFP

About The College Insights

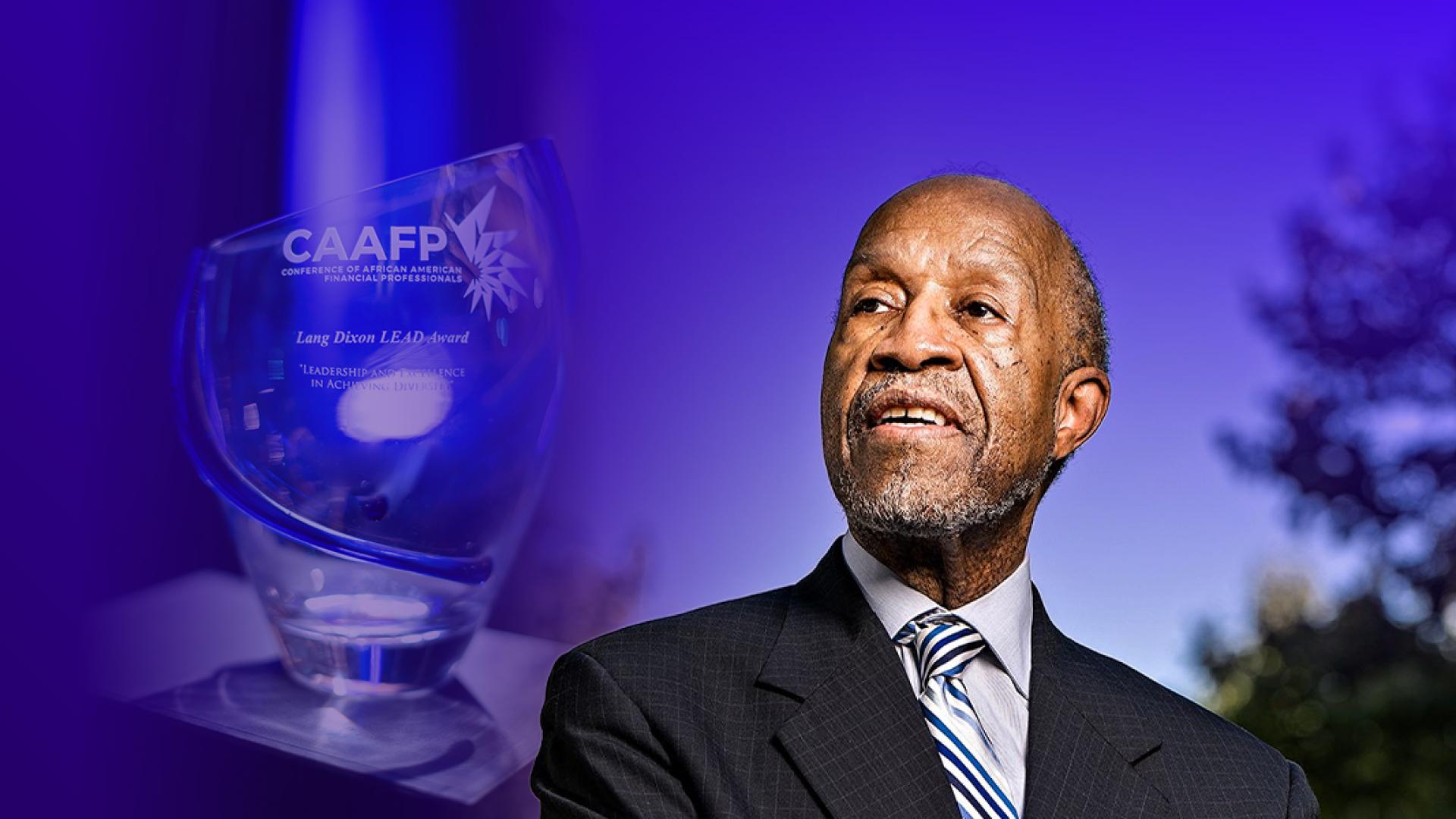

2025 lang dixon award winner

Since 2018, The American College of Financial Services has taken time during the Conference of African American Financial Professionals (CAAFP) to present the Lang Dixon LEAD award to individuals who have significantly impacted the profession of financial services. This year’s recipient, , MBA, CFP®, has earned this recognition over a lifetime of achievement that includes becoming the first African American to earn the CFP® certification in 1978, founding the Association of African American Financial Advisors, serving as a lecturer at Howard University, and more.

Though CAAFP focuses on the strength of the financial services community and emphasizes the importance of collective impact, it is also important to recognize the accomplishments of leaders such as Davis for the impression they have left on the profession. Without Davis blazing the trail for African American financial professionals to come, the financial services industry may not look the same as it does today.

More From The College

- Get key insights for uncertainty with our Advising Through Uncertainty Study

- Explore the American College Center for Economic Empowerment and Equality® mission

- Check out more from CAAFP