PhD, CFP®, MSFP

About The College Insights

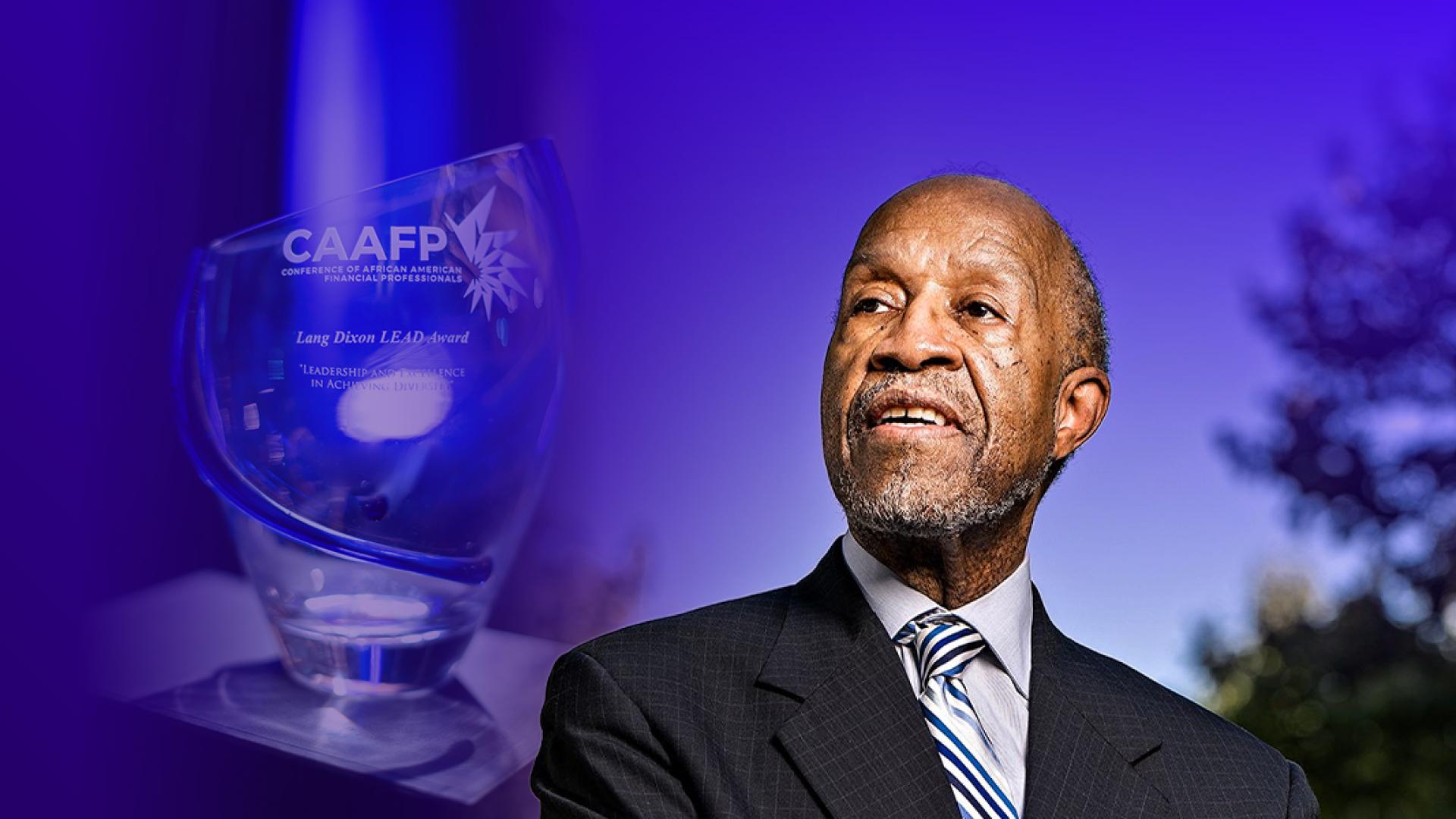

2025 lang dixon award winner

Since 2018, The American College of Financial Services has taken time during the Conference of African American Financial Professionals (CAAFP) to present the Lang Dixon LEAD award to individuals who have significantly impacted the profession of financial services. This year’s recipient, , MBA, CFP®, has earned this recognition over a lifetime of achievement that includes becoming the first African American to earn the CFP® certification in 1978, founding the Association of African American Financial Advisors, serving as a lecturer at Howard University, and more.

Though CAAFP focuses on the strength of the financial services community and emphasizes the importance of collective impact, it is also important to recognize the accomplishments of leaders such as Davis for the impression they have left on the profession. Without Davis blazing the trail for African American financial professionals to come, the financial services industry may not look the same as it does today.

More From The College

- Get key insights for uncertainty with our Advising Through Uncertainty Study

- Explore the American College Center for Economic Empowerment and Equality® mission

- Check out more from CAAFP

Ethics In Financial Services Insights

Ethics & the AI-Ready Workforce

In January 2025, Nationwide Financial Chief Technology Officer and Senior Vice President Michael Carrel participated in the Twenty-Fourth Annual Mitchell/The American College Forum on Ethical Leadership in Financial Services, where leaders and academics discussed how companies are integrating business and ethics considerations in their strategic discussions on responsible AI.

In his reflections, Carrel highlights three key takeaways:

- Ethical decision making is critical to guide AI integration and build trust.

- Preparing an AI-ready workforce requires continuous education and training.

- Balancing speed with safety ensures responsible, sustainable AI adoption.

More from The College

- Read the full Nationwide article.

- Download the 2025 Proceedings, which explores how companies are navigating the intersection of business and ethics with responsible AI.

JD, LLM (Tax), CPWA®