cb15 resource post

Ethics In Financial Services Insights

It’s a Matter of Trust

Filabi also serves as the executive director of the American College Maguire Center for Ethics in Financial Services. The interview focuses on the findings of the Center’s “Trust in Financial Services” research, published in 2022.

This column was originally published in the Journal of Financial Service Professionals, Vol. 77, no. 2, pp. 37-39. Copyright © 2023 by the Society of Financial Service Professionals. All rights reserved.

cb15 resource post

About The College Insights

Alumni Resources

Whether this is your first designation or another step in your learning journey, you’ve reached an important academic milestone — and we salute you. You’ve also gained access to many valuable tools that can further accelerate your professional growth. You can find the full breakdown of all these resources below.

Professional Recertification Program

As a College designee, you are now part of our Professional Recertification Program (PRP). With your annual renewal fee, you get:

- Free ongoing access to Knowledge Hub+: Your home for CE and just-in-time learning on an on-demand platform

- Discounts to in-person educational events and conferences

- Advisor Toolkits to help you demonstrate your value to clients

- Another pathway to lead generation through a partnership with Couplr.AI

- Creation of a free profile on our redesigned consumer search tool YourAdvisorGuide.com

Log into your Learning Hub profile now to take advantage of these PRP benefits!

Promote Your Accomplishments

There are many ways you can spread the word about your latest designation or certification. Start by logging into your Learning Hub profile to view your award letter on the “My Designations and Certifications” page; then, you can:

- Share your digital badge on social media or in your email signature to showcase your accomplishments

- Frame your credentials! Visit our framing partner for styles, pricing, and shipping options (diplomas delivered separately); Huebner School diplomas are 11x14 inches, and graduate school diplomas are 8.5x11 inches

- Review branding guidelines for promoting your designation

- Get digital and print materials to showcase your commitment to knowledge with your Designation Toolkit

- Show your College pride by browsing our School Store! Choose from a wide selection of high-quality College-branded merchandise including apparel, mugs, travel bags, and more!

Take Your Next Step

Learning never stops — so why should you? Continue your pursuit of lifelong learning with another course or program from The College!

- Review the Designation Overview Guide to see all currently available programs, including how stackable course requirements can help you finish faster!

- Take a deeper look at how The College facilitates your lifelong learning journey and ongoing growth

- See the impact of the designations you’ve received on your peers’ business — and how additional designations can power your growth

- Attend a College event for further opportunities for professional development and networking

Giving Back

If you’d like to pay forward how The College has supported your growth and help other financial professionals do the same — as well as shaping the future of society at large — you can support our mission in various ways:

- Give directly to The College to support a chosen scholarship, Center of Excellence, event, or impact initiative

- Visit our Centers of Excellence to learn more about their missions and engage with them through their programs and events

Learn more about the resources available to you as a valued College alum.

cb15 resource post

cb15 resource post

cb15 resource post

Representation Research

How Can Financial Advisory Firms Prepare for A More Diverse Future?

The Current Situation

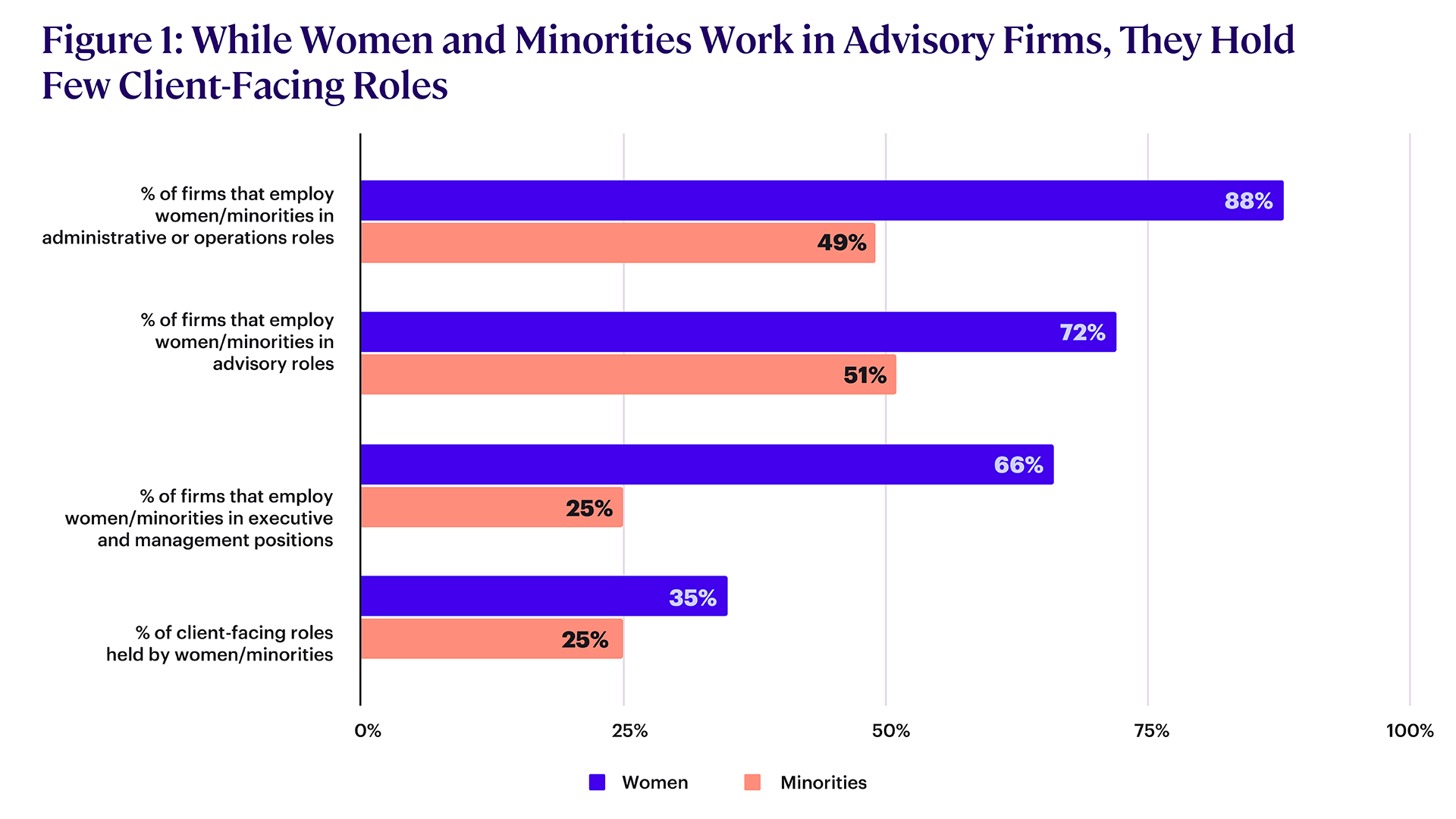

It is no secret that the financial advice industry has remained largely aging, male, and White even as America has grown more diverse, and women and minorities have gained control of a greater share of the nation’s wealth (see Figure 1).

- American women control more than $10 trillion of financial assets.

- Between 2016 and 2019, Black and Hispanic family wealth rose 33% and 65%, respectively, compared to 3% for white families.

The American College of Financial Services. Diversity & Inclusion in Financial Advice 2020. 2020.

As a result, many industry experts worry about the profession’s long-term growth and survival prospects. Unless firms can attract more minority, young, and female practitioners, there is a real risk that the industry will struggle to remain relevant in the decades ahead.

To better understand the factors driving the industry’s lack of diversity and what is needed to promote change, we conducted The American College of Financial Services Diversity & Inclusion in Financial Advice Survey. Here is what we found.

The Roadblocks

Almost 60% of respondents to the survey recognized that lack of diversity is a problem within the advice business. However, relatively few believed that their firms are working to resolve the problem:

- Only 35% said their firm tries to foster racial diversity in its staff.

- Only 36% said their firm works with suppliers committed to diversity.

Our research found that there are several structural factors standing in the way of increased diversity in financial advisory firms.

- Limited Entry Points – Less than 20% of firms used online postings to recruit new advisors, with 44% preferring to use networking. Unfortunately, by relying on networking for new talent, advisory firms tend to replicate the demographic mix of their current advisors and staff.

- Business-building Expectations – Many firms expect advisors to pay for themselves immediately or very quickly. They, therefore, tend to hire already-successful advisors who arrive with their own book of business, which results in no change in the industry’s demographics. Firms also often expect new advisors to rely on their own network of affluent investors to build a book of business and generate leads, which disadvantages candidates from less privileged backgrounds who do not have a network to tap.

- Lack of Transparency in Distributing Sales Leads – While 60% of advisors felt leads and new clients were distributed fairly at their firm, 71% of firms lack a visible process for distributing leads. With limited transparency and accountability in how leads are distributed, women and minority advisors may find themselves at a disadvantage.

The Solution

There are many actions that firms can take to accelerate their diversity efforts, including: Appoint an executive with formal responsibility for diversity. Developing mentoring programs. Implementing collaborative conflict resolution procedures. Allowing anonymous reporting of harassment. Setting formal workforce diversity goals. Offering diversity education and training. Establishing a diversity committee.

To learn more about how well these and other strategies work and how your firm can implement them, download the full survey results today.

cb15 resource post

cb15 resource post

cb15 resource post